This type of gift arrangement allows you to direct gifts to the Archdiocese for a specified period of time and, in turn, receive either a charitable deduction now for gifts made in subsequent years or a reduction in gift or estate taxes on property you wish to pass to heirs.

Under the nongrantor plan, you irrevocably transfer assets to a trustee and provide that payments be made to the Archdiocese of New York for a certain number of years (or until the end of your or another’s life). Then the principal is distributed to your children, grandchildren, or other heirs. The principal passes to your heirs at greatly reduced gift- and estate-tax rates and sometimes escapes them altogether. The charitable lead trust may appeal to individuals who wish to make a gift but retain the property in their family.

Charitable lead trusts (CLTs) are simple in concept but are complex gift- and estate-planning devices because of the many technical drafting requirements of the IRS. We recommend you consult an attorney who specializes in trusts and estates and has experience with CLTs.

There are two types of charitable lead trusts: the grantor lead trust and the more popular nongrantor lead trust, which was made famous by the late Mrs. Jacqueline Kennedy Onassis.

Most donors who use CLTs to accomplish their philanthropic and estate-planning objectives opt to create a qualified CLT. Many requirements must be met for a CLT to be qualified, but here are a few major considerations:

- The payments (gifts) to the Archdiocese must be an annuity interest (fixed-dollar amount annually) or unitrust interest (fixed percentage of the fair-market value of the trust assets determined annually). There are no minimum or maximum payout rates.

- The term of the trust (the number of years in which gifts will be made) must be measured by the life or lives of a person or persons living when the trust is created or a specified number of years.

- The charitable beneficiary must be an organization described in the appropriate sections of the IRS Code. The Archdiocese of New York is a qualified charitable organization.

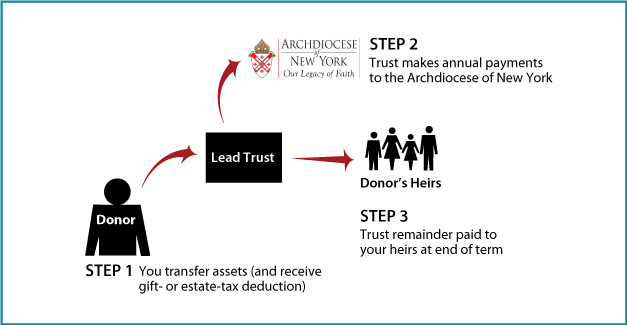

Nongrantor Lead Trust

How It Works

- Create trust agreement stating terms of the trust (usually for a term of years) and transfer cash or other property to trustee

- Trustee invests and manages trust assets and makes annual payments to the Archdiocese

- Remainder transferred to your heirs

Benefits

- Annual gift to the Archdiocese

- Future gift to heirs at fraction of property’s value for transfer-tax purposes

- Professional management of assets during term of trust

- No charitable income-tax deduction, but donor not taxed on annual income of the trust

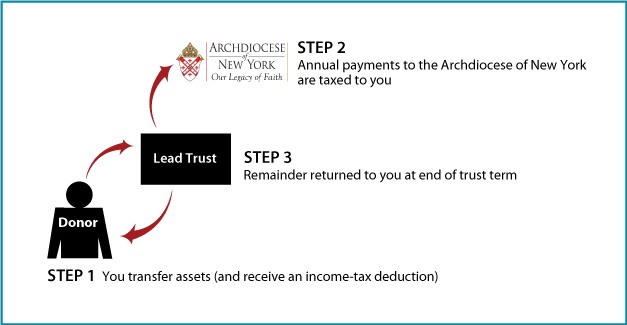

Grantor Lead Trust

How It Works

- Create trust agreement stating terms of the trust (usually for a term of years), transfer cash or other property to trustee, and receive an income-tax deduction

- Trustee invests and manages trust assets and makes annual payments to the Archdiocese

- Remainder transferred back to you

Benefits

- Annual gift to the Archdiocese

- Property returned to donor at end of trust term

- Professional management of assets during term of trust

- Charitable income-tax deduction, but you are taxed on trust’s annual income

Contact Us

| Planned Giving Office 646.794.3317 [email protected] | Archdiocese of New York 1011 First Avenue 14th floor New York, NY 10022 |

© Pentera, Inc. Planned giving content. All rights reserved.